Afghanistan Peace Campaign

Afghanistan Peace CampaignAfghanistan Analysts Network

Afghanistan’s food system is under growing strain. Domestic harvests remain insufficient and uneven and trade routes have shifted repeatedly in recent years. This spring’s rainfall has been good enough for a forecast of a bumper wheat crop, but that belies the ruinous longer-term reality of the climate crisis and the more frequent droughts it is causing. Population growth, returnees and declining purchasing power have all deepened vulnerabilities in both rural and urban areas. In this report, guest author Mohammad Assem Mayar* brings together spatial data on major crops – production, deficits and risks – to show where food is produced, where shortages are emerging and how external shocks – from regional trade disruptions to climate variability – shape the nation’s food supply. He also examines some practical options for increasing production, with a focus on water and irrigation.

Afghanistan has long struggled to produce enough food for its population, a challenge shaped by its mountainous terrain, limited arable land and highly variable precipitation, worsened by climate change. The country came closest to broad food self-reliance between the late 1940s and 1973, following the implementation of ten major irrigation and water management projects that expanded irrigated agriculture and stabilised production in key river basins.[1] These systems added 332,800 hectares of irrigable land and contributed to a period of relative food security in the 1960s, when the population was under ten million. This brief stability ended with the political upheavals and decades of conflict that followed, leaving the country once again dependent on imports and vulnerable to climatic shocks. Since then, Afghanistan’s population has reached an estimated 43.8 million in 2025 (UNFPA), with no systematic expansion of arable farmland.

Afghanistan’s food economy is defined by a persistent gap between domestic production and the population’s needs. Even in years of good rainfall, harvests fall short of national needs for nearly all staple foods, particularly wheat and rice. The country faces a multifaceted food crisis driven by the convergence of multi-year droughts, the devastating economic collapse following the 2021 political transition (World Bank),[2] the 2022 poppy ban and the forced return of 5.4 million Afghans from Pakistan and Iran since 2023 (UNHCR). These pressures are compounded by a decline in purchasing power across both rural and urban populations, leaving millions unable to afford basic staples even when markets remain supplied through imports. Meanwhile, a significant reduction in humanitarian aid since 2022 has widened this gap, removing a key safety net for millions of vulnerable households.[3]

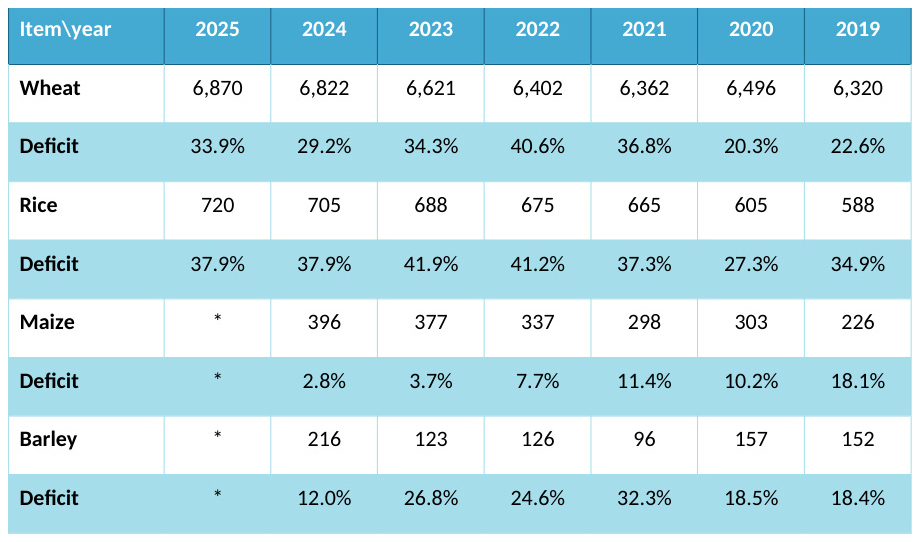

Understanding the depth of this fragility requires looking at the structure of Afghanistan’s food economy. Afghan diets are heavily cereal-centric, with wheat providing most of daily calories for most households. This creates a ‘wheat gap’ – the difference between national demand (around 6.9 million metric tonnes) and average domestic production, which rarely exceeds 4.5 to 5 million tonnes. Agricultural production is uneven across regions. Irrigated northern and northeastern provinces serve as the national breadbasket, while the rainfed belts of the west and the northern highlands are frequently exposed to climate shocks, including recurrent droughts.

According to the latest Integrated Food Security Phase Classification (IPC) analysis, an estimated 17.4 million Afghans faced food insecurity, including 4.7 million at IPC Phase 4 (Emergency) levels during the most recent ‘lean season’ (November 2025–March 2026). Some seasonal improvement is expected between now and September, as harvests come in (the forecast was for 13.8 million in food insecurity, including 2.9 million at emergency level) and that improvement should now be even greater than predicted (as shown in the IPC projection for April – September 2026). The IPC’s first projection was carried out in October 2025, before good spring rains fell. Combined with the Islamic Emirate of Afghanistan (IEA’s) poppy ban, that is pushing poppy farmers into wheat, the rain may mean Afghanistanrecording one of its largest wheat harvests in decades. Significantly, the rains were unusually well distributed, raising expectations of a strong rainfed wheat harvest for the first time in several years. The rain is also good news for farmers of other crops and livestock farmers.

Climate signals also point to a potentially favourable year ahead. A transition toward a strong El Niño in the Pacific is expected to bring above‑average winter precipitation and colder temperatures for Afghanistan, suggesting another year of good water availability for agriculture (if predicted conditions persist until spring 2027). However, this good news sits atop long‑standing structural constraints, especially those relating to climate change. It is already causing more frequent and more severe droughts.

This report addresses a central question: Can Afghanistan feed itself? This raises an important related issue – food security – whether all households in Afghanistan can feed themselves, given widespread poverty, weak purchasing power and uneven access to land and markets? As elsewhere, food security is shaped by broader social, political and economic factors, including who owns land, who has access to water and to capital, who controls trade and market prices and what social relations underpin farming and trade. National production alone does not guarantee food security.However, it does provide a useful starting point for analysing how Afghanistan’s food system functions and is the focus of this study. A second question is whether Afghanistan should aim for greater self-reliance in food production or continue to rely on food imports. Food imports are also vulnerable to economic and political shocks.

This report starts by mapping Afghanistan’s food deficit and explaining how it is measured. It then examines domestic production levels and the risks farmers face, before taking a detailed look at the main crops and meat production. It looks at the approaches taken by the Islamic Republic and Islamic Emirate to increase food production.

The report then briefly examines two other sources of food – imports and humanitarian food aid – and considers the problems both are facing. Finally, it ends with some practical measures to increase domestic production. Given the historical importance of irrigation, and drawing on the author’s expertise in water management, particular attention is paid to water as a key factor in increasing Afghanistan’s national production of food.

Afghanistan’s food production deficit

Afghanistan’s food deficit is most evident in staple foods, particularly wheat and rice, where domestic harvests consistently fall short of national requirements, even in years of good rainfall. Wheat and rice show the largest deficits, while fruit is the only category that produces a surplus. Table 1 summarises estimated demand and deficits for the main cereal crops based on the Ministry of Agriculture annual reports for 2024, 2023, 2022 and 2021. MAIL also publishes separate wheat and rice reports, including those for 2025, which are available here and here, respectively.

While these figures highlight the scale of the deficit, understanding them requires a brief explanation of how production is measured.

How is domestic production measured?

Mapping Afghanistan’s complex agricultural sector or its multifaceted food system is a formidable task. This analysis focuses on the main staples that form the backbone of the Afghan diet, locally called dastarkhan: wheat and flour, rice, maize, legumes, meat, fish, cooking oil, fruit and vegetables. It draws on data from the Annual Agriculture Reports published by the Ministry of Agriculture, Irrigation and Livestock (MAIL); the National Statistics and Information Authority (NSIA) annual Trade Statistics Yearbook, which provides official data on imports and exports; and United States Department of Agriculture (USDA) statistics.

Wheat production is estimated using a combination of satellite‑based mapping and administrative reporting. Each year, Ministry of Agriculture analyses Sentinel‑2 imagery (with 10-metre spatial resolution) to determine the total area planted with irrigated and rainfed wheat, using Normalised Difference Vegetation Index (NDVI) signatures, a proxy for crop health, to distinguish crop cover from other land uses. To refine yield assumptions, remote estimates are combined with field‑level observations on crop condition, rainfall and pest damage from provincial agriculture departments. Total production is calculated by multiplying the estimated area by yield factors, which vary by province and by irrigated and rainfed zones.[4]

Rice production is estimated using a similar approach, but with greater reliance on irrigation mapping. Because rice is grown in flooded fields, satellite imagery can more easily identify rice paddies during the transplanting and peak vegetative stages, when spectral signatures are most distinct. Provincial agriculture offices submit production estimates based on field visits, which are cross‑checked against remotely sensed data, before national totals are calculated.

For other major crops, including maize (corn), legumes and fodder grains, the Ministry of Agriculture uses a lighter but consistent methodology. Satellite imagery is used to estimate cropped areas, although distinguishing these crops spectrally is more difficult than for wheat and rice. As a result, the Ministry of Agriculture supplements remote sensing with provincial reporting, which provides area and yield estimates based on local field inspections. Yield assumptions are anchored in the ten‑year baseline and adjusted for rainfall, irrigation access and reported pest or disease outbreaks. In the absence of nationwide surveys, the production figures are a synthesis of remote sensing, provincial reporting and historical baselines.

Domestic production: levels and trends

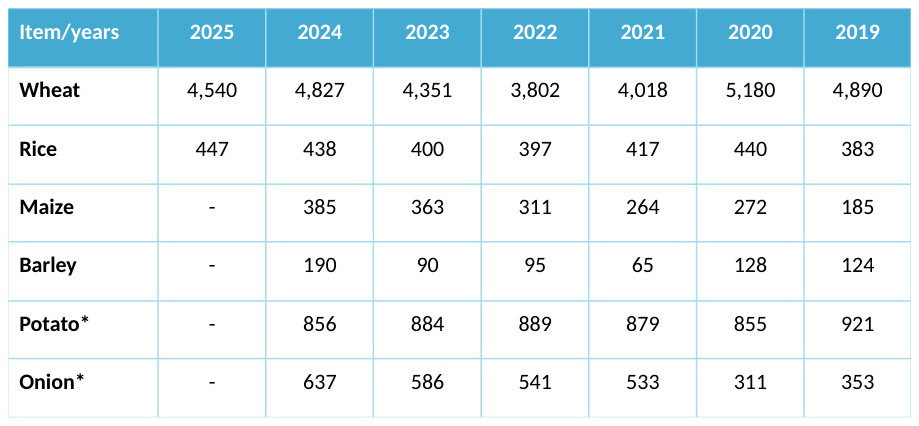

While Table 1 shows the scale of national deficits, Table 2 presents domestic production levels using the Ministry of Agriculture’s reporting for 2024, 2023, 2022 and 2021.[5] Much of the variation is driven by the weather: 2019 was a ‘wet year’, with above-average precipitation; 2020 was broadly normal; and 2021 to 2024 were affected by drought. In addition, the 2022 poppy ban affected wheat production in the subsequent years.

These production patterns cannot be understood in isolation, as they are shaped by a range of structural and climatic risks.

Risks to food security

Afghanistan’s food system faces a wide range of overlapping risks – from climate-related shocks to socio-economic vulnerabilities – that affect both production and access to food. Drought remains the dominant pressure, particularly in rainfed areas, but other shocks also play a role.

Fruit cultivation has proved more resilient than cereals and livestock. However, spring floods and flash floods regularly destroy cropland, orchards and irrigation infrastructure. While their impact may be small on the national scale, they can wipe out a household’s or a village’s annual food supply. Heatwaves and warm winters trigger early flowering, leaving orchards vulnerable to late frosts.[6] Hailstorms can also damage blossom and fruit in orchards – which are vulnerable because Afghanistan lacks protection nets – as well as other crops.

The livestock sector, which depends heavily on pasture, has been hit hard by climate change, with fodder shortages and periodic disease outbreaks forcing distress sales. Herd sizes have declined, especially in rainfed provinces such as Badghis, Ghor, Faryab and parts of the south.[7] Cold waves and colder-than-average winter temperatures also lead to livestock losses. For instance, livestock losses ranging from 70,000 to 200,000 in Ghor province from December 2022 to January 2023, according to the Food and Agriculture Organization of the United Nations (FAO).

Locust outbreaks, particularly in drought years when the collapse of rainfed pasture creates ideal breeding conditions, have historically affected the northern provinces, but can spread into irrigated zones.

Meanwhile, the return, to date, of 5.4 million Afghans from Pakistan and Iran since 2023, combined with a high birth rate, means population growth continues to outpace food production. After the economic collapse in 2021, household incomes and purchasing power fell in both rural and urban areas, reducing the ability of millions of Afghan households to buy basic staples, even when markets remain well supplied. Trade disruptions, including border closures with Pakistan and global price spikes linked to the wars in Ukraine and the Middle East, have further increased the cost of food imports.

Taken together, these pressures create a food economy that is chronically stretched, structurally import-dependent and highly sensitive to both climate and market shocks.

Domestic production by crop

These climatic and structural pressures shape agricultural production in different ways across crops and regions. The following subsections examine Afghanistan’s major crops and meat production, focusing on harvests, deficits, regional distribution and seasonality.

Wheat

Wheat is the backbone of Afghanistan’s national food supply, dominating both cultivated land and caloric intake. Wheat is harvested from June (Jawza) to September (Sunbula), with the lean period stretching from February (Dalw) to May (Saur).

Wheat is grown in all provinces, but production is uneven, shaped by geography and water availability. Between 2019 and 2025 (1398-1404), annual harvests fluctuated between 3.8 and 5.1 million tonnes. The 2025 (1404) season yielded 4.54 million tonnes, a decline driven almost entirely by the collapse of rainfed (lalmi) production due to drought. While the geography of production has not changed and the irrigated wheat harvest in provinces such as Kunduz, Takhar, Baghlan, Helmand, Kandahar and Farah have remained relatively stable, rainfed harvests – especially in Badghis, Faryab, Jawzjan, Baghlan and parts of Takhar – have suffered from drought and erratic rainfall (Figure 1).

In wetter years, more provinces produce wheat surpluses (highlighted in green in Figure 2), while others, including Kabul, Daikundi, Bamyan, Nuristan and Panjshir (highlighted in orange), remain in deficit.

In addition to the impact of drought, Figure 3 also shows how the 2022 poppy ban has reshaped wheat production: by 2023, most poppy fields had been converted to wheat, increasing the harvest, despite persistent drought, particularly in Helmand – previously the country’s largest opium-producing province – where, according to Alcis estimates, 98 per cent of land previously under poppy cultivation was instead sown with wheat.

Rice

Rice is the second most important staple after wheat, with production relatively stable, ranging from 383,000 to 447,000 tonnes between 2019 and 2025. Cultivation is concentrated in Kunduz, Takhar, Baghlan, Nangrahar and Laghman. Together, they account for most of the national output, while provinces such as Sar-e Pul, Bamyan and Uruzgan contribute negligible amounts (Figure 4).

Rice is almost entirely dependent on irrigation, making it highly vulnerable to water shortages. Harvesting typically occurs from October (Mizan) to November (Aqrab), with shortages most visible in early spring and summer.

Both maps below (USDA on the left and MAIL on the right) show the provinces where rice is grown. The variation, which may be due to methodology, is negligible.

Maize

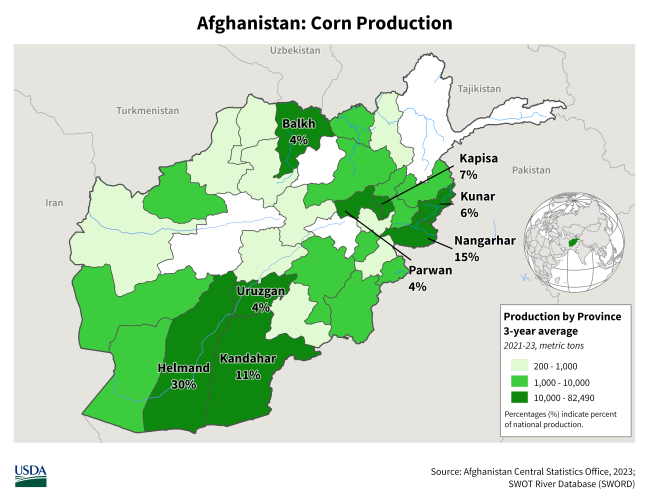

Maize is widely cultivated, primarily as a feed crop. National production has ranged between 185,000 and 385,000 tonnes in recent years. The strongest producers are Helmand, Kandahar, Balkh, Nangrahar, Kunar and Kapisa, while the northern highland provinces, such as Sar-e Pul, Jawzjan and Faryab, also contribute a little (Figure 5). Because maize is planted after the wheat harvest, it depends heavily on residual soil moisture and the availability of irrigation. Seasonal availability peaks in August and September (Asad and Sunbula), but shortages mainly affect livestock feed and poultry production, rather than household food security.

Barley

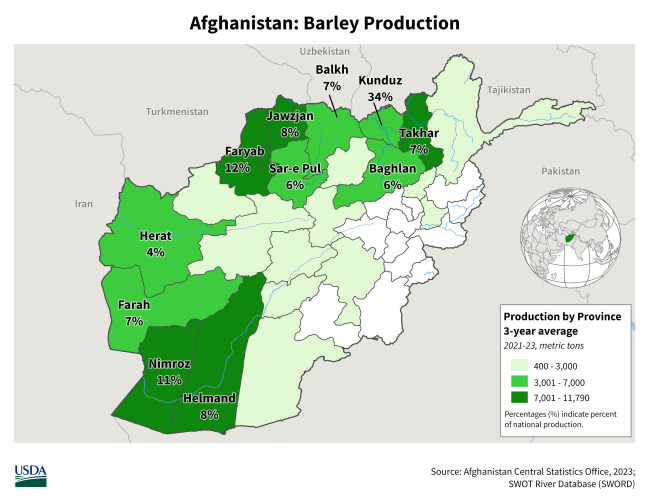

Barley is typically planted in the same agro-ecological zones as rainfed wheat, meaning it faces similar drought exposure. Production fluctuates from year to year – ranging from 65,000 tonnes in 2021 to 190,000 tonnes in 2024, reflecting its concentration in drought-prone rainfed zones and its sensitivity to moisture stress. In provinces such as Badghis, Faryab, Jawzjan and parts of Ghor, yields can collapse in dry years. Barley plays an important stabilising role in both household consumption and livestock feed, particularly in years when wheat production declines. Poor harvests have cascading effects: reduced availability of animal feed increases pressure on already weakened herds, especially in regions where pasture degradation is widespread

The spatial distribution of barley, shown in Figure 6, using USDA estimates, shows the strongest concentrations in the northern and western rainfed belts.

Vegetables (potatoes and onions)

Potatoes and onions are key staple vegetables grown for both household consumption and market sale. They are valued for their storability and role in bridging gaps in the lean season, from February to May (Dalw to Saur), when fresh produce is scarce.

Potato production is concentrated in the cool highland provinces – Bamyan (the country’s potato hub), Daikundi, Ghazni and parts of Wardak – where the climate favours tuber crops. Their high yield per hectare also makes potatoes an efficient crop for land-constrained highland communities.

Onion cultivation is more widespread but depends heavily on irrigation. Major producing provinces include Kandahar, Nangrahar, Balkh and Kunduz, supplying both domestic markets and Pakistan and India. Prices are seasonal, falling during the harvest months (Asad to Mizan) and rising in winter and early spring due to storage losses. Limited cold-storage continues to drive post-harvest losses, reducing incomes and contributing to price volatility.

Legumes

Pulses, including chickpeas, lentils and mung beans, remain a small but nutritionally important component of agriculture, accounting for only a fraction of the national caloric supply.

Yields vary by crop and year, due to climate factors, pests and the size of the area under cultivation (see Figure 8 for 2021). Production is concentrated mainly in Balkh, Baghlan, Kunduz, Herat and Faryab provinces, with smaller-scale cultivation in the central highlands, mostly for local consumption. Pulses are typically harvested from July to September (Saratan to Sunbula), with market availability improving in early autumn. Their contribution to national food security is limited by both low acreage and the absence of large-scale processing.

Oilseeds

Oilseed cultivation is scattered across irrigated zones in the north, northeast and south, with crops such as sesame concentrated in Nangrahar and parts of the north, sunflower in Balkh, Kunduz and Jawzjan and cottonseed in Kandahar, Helmand, Baghlan, Kunduz and Balkh.

For generations, households relied on dairy-based butter and ghee, or oil extracted from locally grown oilseeds. While these practices continue in some rural areas, most cooking oil is now imported. Domestic production from sunflower, sesame and cottonseed, along with small amounts of safflower, falls well short of national demand, making cooking oil one of the most import-dependent components of the Afghan diet.

Processing capacity is also limited. A small number of local factories produce oil from cottonseed and other oilseeds, particularly in northern provinces, although TOLOnews recently reported on a modern factory with a 200-tonnes-per-day production capacity in Kandahar.

Fruits

Fruits are a major source of rural income and – unlike cereals – consistently exceed domestic demand, making them a cornerstone of export earnings (Figure 9). Major crops include grapes, apricots, almonds, apples and pomegranates, produced across different agro-ecological zones, with grapes having the largest share of total fruit output, followed by apricots, almonds, apples and pomegranates (For the quantity and proportional share of each fruit in the various areas under cultivation, see the MAIL reports.)

Grape strongholds in Kandahar, Helmand, Herat, Balkh and Samangan are supported by established vineyards and raisin processing facilities. Apricot production is also substantial, particularly in the northern provinces and the central highlands. Fresh and dried apricots contribute to household incomes and export. Almonds, which show strong harvests in Kandahar, Uruzgan, Zabul and Samangan, remain one of Afghanistan’s most valuable horticultural exports. Apple production is concentrated in the cooler highland provinces, with Wardak, Ghazni, Bamyan, Paktia and Logar producing most of the national supply. Pomegranate production is strong in Kandahar, Helmand, Farah and Kapisa. It remains a major export commodity, with stable yields despite water shortages. Figs, peaches, mulberries and walnuts contribute smaller but steady quantities to the national fruit supply. These crops are important for local consumption and small-scale trade.

Melons, including watermelons, are among Afghanistan’s most widely consumed seasonal crops, with significant production volumes. Major melon producing provinces include Farah, Helmand, Balkh, Kunduz, Baghlan and Nangrahar, which supply markets from July to September (Saratan to Sunbula). Watermelons are grown under both rainfed and irrigated conditions and are therefore affected by drought. Afghan melons, particularly the Kunduz and Mazar varieties, are valued for their storability and sweetness.

While fruit production is relatively stable, storage constraints and water shortages affect quality and market access.

Meat

Although MAIL appears to publish periodic livestock assessments, the author could access only one annual livestock report – for 2020 – which provided provincial estimates for major livestock categories (sheep, goats, cattle, horse, chicken and other poultry).

In the absence of consistent annual reporting, meat, poultry and fish production figures are often released through press releases or media reports. For example, Afghanistan produced an estimated 1.5 million tonnes of beef and mutton in 2021 (MAIL) and the country’s 10,000 poultry farms were producing a reported 1,700 tonnes of chicken meat per day in 2024 (Pajhwok).

Aquaculture is expanding, with more than 2,600 active fish farms in provinces such as Nangrahar, Kunduz, Balkh and Herat (Ariana News). However, fish consumption accounts for only a small share of the country’s protein consumption, and output remains below demand, which peaks in winter.

Availability is highly seasonal, with drought and pasture degradation reducing herd resilience, leading to year-to-year fluctuations, while winter months always bring tighter supplies and higher prices as fodder becomes scarce.

Mapping Afghanistan’s food deficits makes it very clear that the country cannot feed itself, but is there potential for it to do better? The following section considers government actions over the last quarter century which have aimed at increasing Afghanistan’s capacity to grow more of what it eats.

Government actions

State responses to Afghanistan’s food security challenges have evolved over time, reflecting changing political systems, institutional capacities and external support. The following sub-sections examine how successive governments have sought to increase Afghanistan’s food security.

Under the Islamic Republic

During the relatively stable period of the Republic (2001-21), the government introduced a range of strategies aimed at improving food production, nutrition and agricultural resilience, but was unsuccessful in closing food deficits. Most of these measures date from the Ashraf Ghani governments, including the Wheat Sector Development Strategy, the National Comprehensive Agriculture Development Priority Program (NCADPP), the Food Security and Nutrition Strategy, the Afghanistan Drought Risk Management Strategy, the National Irrigation Investment Roadmap, 2020-30 (seen by the author), alongside efforts to reform the Ministry of Agriculture to a more decentralised, farmer-oriented institution (as part of the ministry’s Comprehensive Agricultural Development Programme -archived on the Wayback Machine).

These strategies were supported by extensive donor-funded programmes, including the On-Farm Water Management Project, and the Afghanistan Agriculture Inputs Project (AAIP), both funded by the World Bank; the IFAD-supported Community Livestock and Agriculture Project (CLAP); and climate-related initiatives such as the Climate Change Adaptation Project (CCAP) and the Community-Based Agriculture and Rural Development (CBARD), funded by the Global Environment Facility (GEF). Additionally, the European Union and the Asian Development Bank supported several watershed management and irrigation programmes, in the Kunduz, Amu and Panj river basins.

In parallel, the Republic-era Ministries of Energy and Water and Agriculture initiated a number of water infrastructure projects, including the Kamal Khan Dam in Nimruz province, Shah wa Arus Dam in Kabul, Pashdan Dam in Herat; the Zamin Dawar and Musa Qala Canals in Helmand province; diversion tunnels for the Bakhshabad Dam in Farah province, the Kama Barrage in Nangrahar province; the Shahi Canal in Laghman province; and the Qush Tepe Canal in Balkh province.[8] Progress, however, varied and the Kamal Khan Dam was the only major project largely completed before 2021, although several were later continued, some of them to completion, by the Emirate. While these projects have the potential to improve water management, their impact on expanding arable land has so far been limited.

Launched in 2017, the Afghanistan Food Security and Nutrition Agenda (AFSeN‑A) aimed to provide a multisectoral framework for addressing hunger and malnutrition. Its practical impact was limited, beyond aligning Afghanistan with the UN’s Sustainable Development Goals: 2 (Zero Hunger) and 17 (Partnerships). AFSeN-A effectively ended after the fall of the Republic, continues to influence the government’s reporting systems and UN programming (see for example FAO’s agricultural sector strategic roadmap, 2026–2028).

Despite all these plans, technical support and donor funding, little was achieved to actually increase food production during all the years of the Republic, a problem familiar in almost all sectors of the economy and government.[9]

Under the Islamic Emirate

Since 2021, the IEA has continued and completed several infrastructure projects initiated under the Republic, including Shah wa Arus Dam, (Amu TV), the diversion tunnels of the Bakhshabad Dam in Farah (Al Emarah) and work on the Pashdan Dam in Herat (The Diplomat), as well as phase II of the Qush Tepa Canal (Bakhtar). Smaller projects, including the Shahi Canal and several dams, remain under development or are focused primarily on drinking water supply, with limited impact on irrigation or agricultural expansion.

The Emirate has also moved to revive state‑owned grain infrastructure, including reopening government‑owned silos that had long been inactive (Hasht-e Subh). Wheat will be purchased during harvest and released later to help stabilise prices (The Kabul Times), although the scale of this initiative remains unclear. Official statements have also highlighted Afghanistan’s fast approach to self-sufficiency in poultry – 80 per cent in 2019 and, more recently, 99 per cent in 2025. According to a Ministry of Agriculture official, who asked not to be identified, the country is now largely self-sufficient in poultry but still relies on imported breeding stock. The Emirate has also started exporting sheep meat to Central Asia to curb the smuggling of lives animals to neighbouring countries and incentivise private-sector investment in livestock production.

Achieving major improvements in food production will be difficult. The Emirate is hamstrung in what it can achieve in terms of developing irrigation and other projects aimed at improving agricultural production. International aid has focused on humanitarian efforts since 2021 (for political reasons and a political impasse between donors and the Emirate, AAN).

The Emirate has limited resources to spend on development, partly because it concentrates funding on the security services. The March 2026 World Bank Economic Monitor reported that 48 per cent of spending in financial year 2025 (ending 20 March) went to the army, police and intelligence and just 1.6 per cent on agriculture (figures from the Emirate Ministry of Finance). The Emirate is now putting a greater portion of the budget into capital spending, rather than running costs (largely wages) and capital spending has tended to focus on water management projects, especially the Qush Tepa Canal. It is also increasing, albeit from a very low level.[10]

It is also worth mentioning that immediately on taking power, the Emirate introduced agricultural taxes – ushr (a tithe on the harvest) and zakat (a wealth tax, usually taken on livestock), which is collected by the Ministry of Agriculture and delivered to the Supreme Leader’s Office, ie it does not go into the general budget via the Ministry of Finance (in most Muslim countries, these are given as personal acts of charity, rather than taxes taken by the state).[11] While this measure may not affect national production, it may hit the food security of individual households and communities.

The next section looks in detail at one technological intervention as an example of how interventions can bring costs as well as benefits. The solar‑powered borehole is a relatively new technology that has spread rapidly across Afghanistan in recent years, without any push, or indeed, any control by the state, whether the Republic or Emirate. Greater state intervention here would have been helpful.

Agricultural expansion by groundwater and its limits

In recent years, unregulated solar-powered boreholes that extract groundwater at low cost have spread widely across the country, helping farmers cope with drought and expand irrigated agriculture.

Although their contribution to national production has not yet been systematically quantified, their output is already included in official production figures.

In 2023, NSIA reported around 310,000 boreholes nationwide; FAO identified far more in 2025 – 489,314 solar-equipped boreholes in 32 provinces, indicating a sharp increase, particularly in 2023 (Figure 10).

The distribution of boreholes is highly uneven, with the largest concentrations in Helmand, Kandahar and Farah. In these areas, they have enabled the rapid conversion of previously uncultivated desert land into irrigated fields, much of which was used for poppy cultivation. Following the 2022 poppy ban, many of these areas shifted to wheat – a crop that requires more water but generates less income per hectare. The Alcis map illustrates the scale of land-use change for Helmand and Kandahar, showing large tracts of former desert (considered state property) now under surface irrigation (see here).

While this expansion has supported agricultural growth, it raises concerns about long-term sustainability. If groundwater is extracted faster than it is replenished, water levels drop, making such easy extraction a finite and ultimately counterproductive solution. Reports suggest this is already happening (Yale Environment 360), but comprehensive national data remains limited. There are reports of entire villages being abandoned in Helmand province’s Washir district and in Nawabad, Farah province, due to water scarcity stemming from borehole activity and declining precipitation (see TOLOnews from June 2023 and this August 2023 documentary). Boreholes have also been dug in northern Afghanistan, contributing to a gradual decline in groundwater levels, although the situation there remains stable.[12]Possibly in response to the depletion of groundwater, in 2023, the Emirate introduced an anti-land-grabbing law that, as well as affecting urban areas, restricts further agricultural expansion onto public land, particularly in desert areas. It requires farmers who are already using public land to pay rent or risk losing access to it.

Failing to grow enough food itself, Afghanistan has relied, instead, for decades on food imports and humanitarian food aid to fill the deficit, but as the next sections outline, both sectors are under strain from global instability and cuts to aid.

Trade: imports and shifting corridors

Afghanistan meets its domestic supply gap through imports, particularly for wheat, flour, rice and cooking oil.[13] In 2024, wheat and flour alone accounted for a significant portion of food import volumes and value, underscoring the country’s dependence on imports.

For decades, Pakistan served as the country’s primary food import corridor, including wheat flour from mills in Khyber Pakhtunkhwa, rice from Sindh and vegetable oil through Karachi’s ports. However, repeated border disruptions (New York Times) have translated into immediate price spikes in Afghan markets and Afghanistan has turned to Central Asia as an alternative.

The shift away from Pakistan has been building over time. From 2015 onwards, Pakistan used border closures as a political lever, prompting Afghan traders to seek alternatives. It accelerated as the war in Ukraine disrupted global wheat flows, reducing Ukrainian wheat exports to Pakistan and tightening regional flour supplies (BBC). India’s subsequent suspension of wheat exports further tightened global markets and drove up prices (BBC). As Pakistani mills faced shortages, traders in Pakistan began buying Afghan wheat during the harvest months – particularly from the southern provinces – and exporting it back across the border. In response, the Emirate banned wheat exports in May 2022 to prevent domestic shortages (Ministry of Finance and VOA). By then, the regional supply landscape had already shifted. Finally in October 2025, border closures imposed by the Emirate effectively cut off the route that had once carried mostof Afghanistan’s food imports.

Afghanistan has become increasingly dependent on Central Asia, particularly on Uzbekistan and Kazakhstan for wheat and flour imports. The northern crossing at Hiratan-Termez (Balkh province and Uzbekistan, respectively) has emerged as the country’s new logistical hub for both commercial imports and humanitarian operations. Drought has reinforced this shift: northern provinces that once produced surplus wheat – Faryab, Badghis, Jawzjan and Balkh – are now among those facing crisis-level food insecurity, according to FEWS NET, as shown in Figure 11. As local surpluses disappeared, the northern corridor became the only viable entry point for large-scale wheat imports. The World Food Programme (WFP) and other UN agencies have expanded storage facilities in Termez to ensure rapid delivery to drought-affected regions, replacing the Pakistan-based supply chain that had dominated for decades.

This new dependence on Central Asia comes with its own uncertainties. Relations with Uzbekistan and Kazakhstan are complicated by the Qush Tepe Canal, which diverts water from the Amu Darya and has raised concerns about downstream flows, raising the possibility that political tensions could spill over into trade. For now, however, Central Asia remains Afghanistan’s primary source of wheat and flour.

The rice trade has also been reshaped. Pakistan has traditionally filled Afghanistan’s rice deficit, but border closures and rising political tensions have disrupted this flow, with Indian rice increasingly replacing Pakistani varieties. While Iran plays only a limited role in Afghanistan’s food imports, it has become important as a transit corridor, particularly for imports such as Indian rice entering via Iranian ports in Bandar Abbas and Chabahar and transported overland to Afghanistan.[14] Prices have risen due to longer transit distances and higher transport costs. Traders report that some Pakistani rice is now rerouted through Iran and relabelled as Indian before entering Afghan markets.

Cooking oil imports have also been affected. Previously sourced through Pakistan’s ports, trade has now shifted to Iranian ports and Central Asian suppliers, increasing transport costs. Meat imports have also been affected: buffalo meat from Pakistan, once an affordable protein source, has become scarce, driving up prices in urban markets.

Together, these shifts have made food trade more fragmented, more expensive and more politically exposed.

A supply chain once anchored in a single dominant corridor has now shifted to other routes, shaped by its geopolitical constraints. Amid declining purchasing power, drought and shrinking domestic surpluses, the reconfiguration of trade corridors has become central to Afghanistan’s food economy.

Humanitarian food assistance: coverage, gaps and trends

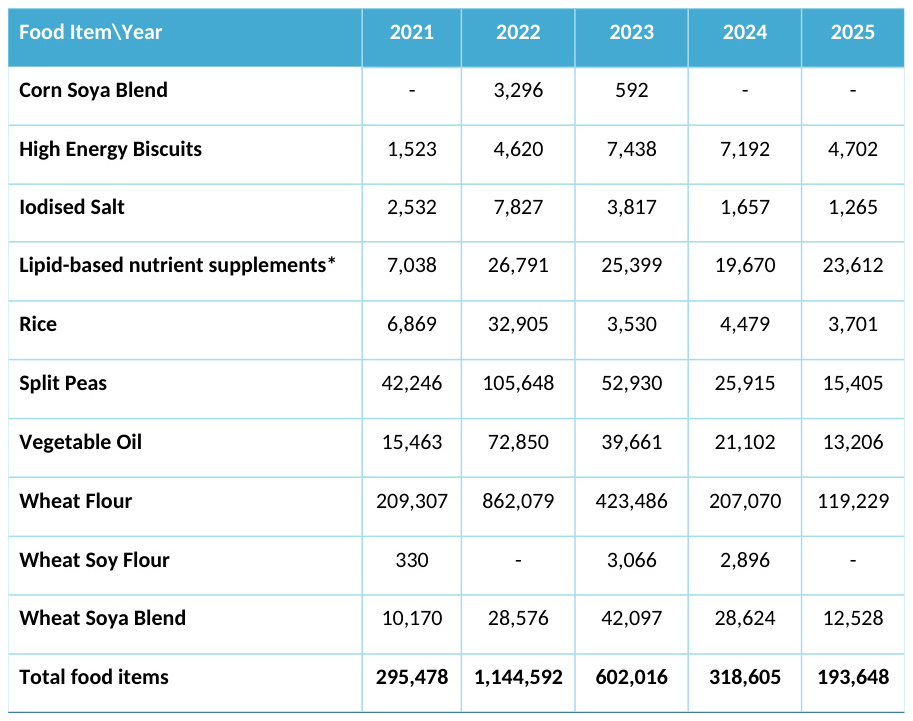

Humanitarian assistance, while intended to be temporary, has become a critical pillar of the food economy, supporting households unable to grow or afford enough food. However, coverage has declined in recent years due to funding constraints. Table 3 summarises the volume of food distributed by WFP between 2021 and 2025 (for details on targeted recipients, see WFP’s annual reports).

The contraction in aid is also reflected in the decline in the number of beneficiaries. In 2022, WFP reached more than 23 million people; by 2025, its coverage had fallen to around 4 million people, plus half a million returnees. This decline has occurred despite continuing high levels of need, with large parts of the country – particularly the northern rainfed belt, the west and pockets of the central highlands – classified by FEWS NET as facing Crisis (IPC 3) or Emergency (IPC 4) conditions.[15]

Changes in aid delivery have had direct effects on markets. Large-scale wheat distributions in 2022 helped moderate price spikes in rural areas, while cash‑based transfers supported local traders and prevented supply gaps (WFP 2022 Afghanistan Country Brief). The subsequent reduction in aid has had the opposite effect: in districts where in‑kind aid distributions were reduced, wheat and flour prices have risen, particularly in drought-affected northern and western regions (WFP Afghanistan 2023 Annual Country Report). Cash‑based transfers, while effective in urban centres, have had limited impact in remote areas where markets are thin.

Coverage remains uneven, with some regions chronically underserved.[16] The northern rainfed belt – Badghis, Faryab, Jawzjan and parts of Balkh and Samangan – has faced repeated droughts and now hosts large numbers of returnees, yet assistance remains inconsistent. The central highlands (Daikundi, Bamyan, Ghor) receive limited support due to access constraints, while in the east, Nangrahar and Kunar have seen assistance decline despite rising needs. FEWS NET has also reported that in some districts, the lack of assistance has pushed households into ‘negative coping strategies’, including distressed livestock sales and reduced meal frequency. Urban areas such as Kabul and Herat receive only limited support despite falling purchasing power.

Ultimately, humanitarian food assistance cannot offset the combined pressures of drought, economic contraction, population growth and declining purchasing power. What was once a stabilising force now reaches fewer people, less frequently and with smaller rations, leaving millions exposed to deepening food insecurity.

The way forward: practical and strategic options

Afghanistan’s food security challenge is shaped less by a lack of agricultural potential than by the country’s political, financial and environmental constraints. While the country has the land, water resources and agro-ecological diversity to increase production, decades of conflict, drought, weak infrastructure, fragmented institutions and the current economic crisis have limited its ability to translate these assets into reliable food production. The way forward does not lie in imagining radically transforming agriculture, but in pursuing practical measures to stabilise production, strengthen resilience, improve access to food and revive the institutions needed to support agricultural planning and rural markets.

In the short term, stabilising wheat production while reducing the country’s exposure to climate-driven shocks remains the priority. Wheat underpins Afghan diets, but it is highly vulnerable because of its reliance on rainfed agriculture in drought-prone regions. Measures such as improving water management, rehabilitating irrigation canals and distributing higher-yielding seeds could help reduce climate‑related losses and improve rural incomes, especially in key irrigated wheat-producing areas such as Kunduz, Takhar, Helmand, Kandahar and Farah.

Meanwhile, some drought-prone rainfed areas may benefit from gradually shifting towards crops that require less water and offer higher returns than wheat. In some areas, such transitions are already underway. In Wardak province, for example, most farmers have shifted from wheat cultivation to apricot and apple orchards that generate higher incomes.

Irrigation and water management will remain central to Afghanistan’s agricultural prospects. Improvements to the country’s irrigation system would reduce the national wheat deficit, but large-scale expansion in the foreseeable future is unlikely given current financial constraints. Large-scale infrastructure schemes, such as the Qush Tepe Canal, require not only funding but also technical capacity, maintenance systems and long-term political stability. A pragmatic way forward would prioritise small- and medium-scale irrigation interventions, such as rehabilitating existing canals, expanding water-harvesting structures and improving on-farm water management. These measures are relatively low-cost, can be implemented in stages and are likely to yield quicker benefits.

Reducing post-harvest losses could also improve food availability without requiring major increases in production. Potatoes, onions, fruits and vegetables are often abundant during harvest periods but become scarce and expensive later in the year because of limited cold-storage facilities and transport corridors. Expanding cold-storage facilities in major production hubs such as Bamyan, Kunduz, Kandahar, Herat and Nangrahar, improving transport networks and supporting local processing could help reduce seasonal shortages and stabilise prices.

In Afghanistan, better food security depends not only on production and infrastructure but also on access to land, water, employment, capital, purchasing power and reliable markets. In their absence, increases in national food stocks alone will not translate into better access to food for households. In that light, food security depends as much on distribution and governance as production.

The decline in humanitarian assistance and the continuing sluggish economy mean millions of households remain highly vulnerable to drought, price rises and other shocks. Prospects for greater food security are shaped by financial, institutional and climatic constraints. While production can be increased in the long term, the country cannot finance the infrastructure needed to close its food gap in the foreseeable future. The narrowing of development aid means the country no longer has access to the financial resources available during the Republic and although the Emirate is clearly interested in agriculture and irrigation, spending priorities – allocating about half the annual public purse to the security sector – limit its capacity to act.

Given current conditions, a realistic strategy should prioritise incremental gains rather than large-scale transformation. Stabilising wheat production, improving water management, reducing post-harvest losses and strengthening market systems are more achievable and likely to deliver lasting improvements in food security. These efforts should be combined with targeted agricultural support, climate finance, regional cooperation on trade and water and investment in irrigation rehabilitation, seeds and nutrition services. Progress will ultimately depend on the consistent implementation of practical, well-targeted, high-impact interventions rather than grand plans.

Edited by Kate Clark and Roxanna Shapour

* Dr Mohammad Assem Mayar is a water resources management and climate change expert and former lecturer at Kabul Polytechnic University in Afghanistan. He is currently an independent researcher based in Germany. He posts on X as @assemmayar1.

References

| ↑1 | In How the water flows: A typology of irrigation systems in Afghanistan, Afghanistan Research and Evaluation Unit, 2008, Bob Rout identified ten major irrigation projects: the Helmand-Arghandab irrigation scheme in Helmand and Kandahar provinces (103,000 hectares of irrigable land); the Sardeh scheme in Ghazni (15,000 ha); the Parwan scheme in Parwan and Kabul (24,800 ha); the Nangrahar scheme (39,000 ha); the Khanabad scheme in Kunduz (30,000 ha); the Shahrawan scheme in Takhar (40,000 ha); the Kelagay scheme in Baghlan (20,000 ha); the Nahr-e Shahi scheme in Balkh (50,000 ha); the Gawargan scheme in Baghlan (8,000 ha); and the Sang-e Mehr scheme in Badakhshan (3,000 ha). |

|---|---|

| ↑2 | For more on the Afghan economy, see AAN’s The Afghan Economy Since the Taleban Took Power: A dossier of reports on economic calamity, state finances and consequences for households. |

| ↑3 | See UNOCHA, Overview of Funding Shortfall and Impact on Humanitarian Operations as of 14 August 2025, the Afghanistan Humanitarian Needs and Response Plan 2026 and the UN Financial Tracking Service (FTS) for data on the decline in humanitarian aid since 2022. |

| ↑4 | Alcis, a UK-based private company, has been using satellite imagery to monitor wheat and poppy cultivation in Afghanistan since 2022. Its data is accessible here. |

| ↑5 | See MAIL’s Annual Agricultural Reports for 2024, 2023, 2022 and 2021. The reports for 2020 and 2019 are not currently available online, but the author previously downloaded them. The FAO Food Balance Sheet (FBS) for Afghanistan (2010-23) provides internationally comparable per‑capita food supply estimates for major commodities, including cereals, pulses, meat, dairy, fruit, vegetables and oils. For Afghanistan, the FBS consistently shows a diet dominated by cereals, particularly wheat, alongside very low per capita consumption of meat, dairy and oils compared with regional and global averages. |

| ↑6 | For more on the impact of climate change on agriculture in Afghanistan, see the author’s AAN report The Economic Consequences of Climate Change for Afghanistan: Losses, projections … and pathways to mitigation, March 2025. |

| ↑7 | Read more on drought risk in Afghanistan, in the author’s AAN report Droughts on the Horizon: Can Afghanistan manage this risk?, February 2021. |

| ↑8 | The Qush Tepa Canal has raised concerns among downstream states, particularly Uzbekistan and Turkmenistan, about its potential impact on the Amu Darya flows. Afghanistan argues that it is using its share of transboundary water resources, while analysts have highlighted risks related to water allocation and sustainability (The Diplomat and Kunduz Adylbekova, Water Crisis Looming: Uzbekistan and Turkmenistan’s Imperative for the Grand Afghan Canal, Central Asian Bureau for Analytical Reporting/Institute for War and Peace Reporting (IWPR) 23 July 2023). |

| ↑9 | For an analysis of why such programmes failed, see Kate Clark, The Cost of Support to Afghanistan: Considering inequality, poverty and lack of democracy through the ‘rentier state’ lens, 29 May 2022, AAN. |

| ↑10 | In its first ‘mini-budget’, for the last three months of financial year 2021 (the only time the Emirate’s Ministry of Finance has released detailed spending figures), 8.7 per cent was allocated to development, although thebudget line was unfunded. The Ministry of Water and Energy had by far the biggest percentage development budget: 673 million afghanis, 76.7 per cent of which was for development. Other ministries ranged from just over 1 to just under 15 per cent) (AAN). In the financial year 2025, the Emirate spent 13.75 per cent of its budget on development, an increase of over a quarter compared to the previous year (World Bank). |

| ↑11 | See AAN, Taxing the Afghan Nation: What the Taleban’s pursuit of domestic revenues means for citizens, the economy and the state, showed (2022), especially pages 37-8, which note that taxation of agricultural products can be problematic for poorer households, even though the very poor should be exempted from such levies. |

| ↑12 | See also the author’s AAN report, Afghanistan’s Urban Water Dilemma: Why are Afghan cities running out of water?, (2025) for the map of boreholes and their status. |

| ↑13 | See NSIA’s Afghanistan Trade Statistics Yearbooks 2024-25, 2023-24, 2022-23, 2021 and 2019 (NSIA has not yet published its 2025 trade report), which are primarily based on ASYCUDA customs records. Afghanistan’s 2024 imports included 272,000 tonnes of wheat (USD 52.67 million); 2.58 million tonnes of wheat flour (USD 680.97 million); 540,942 tonnes of rice (USD 342.68 million); fish (USD 27.98 million); cooking oil (USD 351.5 million) and tea imports valued at USD 65.8 million (green tea) and USD 25.6 million (black tea). |

| ↑14 | Iran exports little wheat because its own domestic needs are unmet. On 3 March 2026, following Israelis and US attacks on the country, Iran imposed an indefinite ban on all food and agricultural exports to protect domestic supplies (Global Food Industry News). |

| ↑15 | See FEWS NET projections for early 2026 and the UN Financial Tracking Service, which documents the decline in annual civilian aid to Afghanistan from a high of USD 3.8 billion in 2022 to USD 1.2 billion in 2025. |

| ↑16 | FEWS NET, Afghanistan Food Security Outlook: October 2025 – May 2026 identifies the northern rainfed belt (Badghis, Balkh, Faryab, Jawzjan, Samangan) as the area of greatest concern due to repeated droughts, high returnee inflows and insufficient humanitarian coverage. |